Diversify Future Income Streams by Choosing between Traditional or Roth IRAs

From Michael Kitces’ Limits Of Tax Diversification And The Tax Alpha Of Roth Optimization.

The Roth IRA and Roth 401k can be an incredibly attractive retirement vehicles, thanks to their ‘unlimited’ potential for generating tax-free growth, at the cost of using after-tax money. Each year households must make a decision whether to contribute to a pre-tax traditional IRA/401k or a tax-free Roth, based on whether the upfront tax deduction (on the traditional contribution) will be more or less valuable than tax-free growth at the end (on the Roth distribution).

When does it make sense to put money in a Roth vs a Traditional Account?

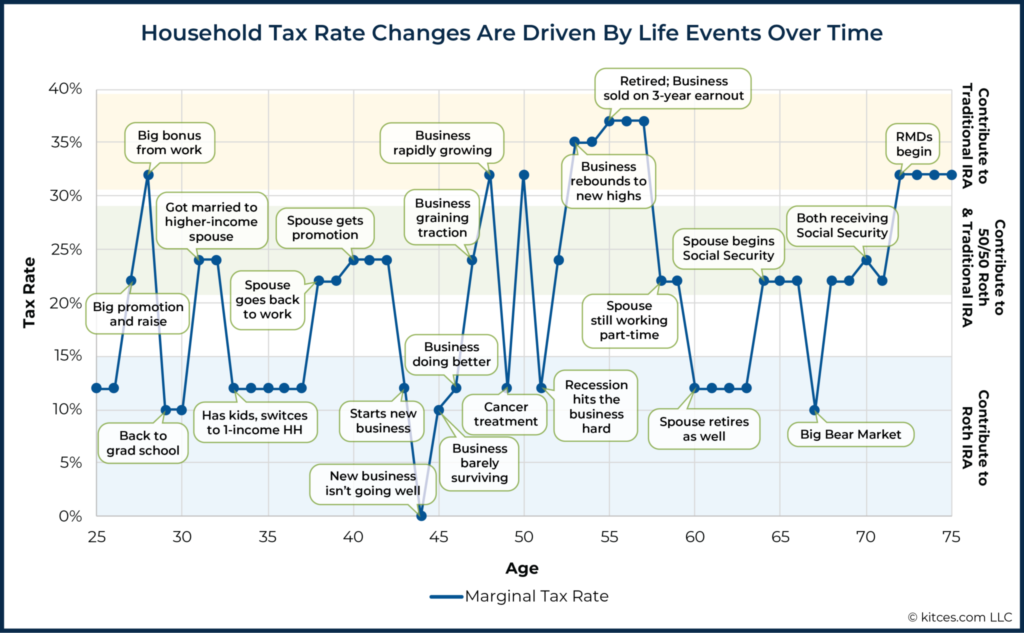

Retirement savers can consider trying to ‘Roth optimize’ by choosing when to add dollars to tax-free Roth accounts. After all, a household’s tax rates typically vary throughout life – often by a wide range as careers start and stop and change, family and health needs impact our time in the workforce and what we earn, businesses are started and subsequently fail or succeed, and eventually retirement comes (with its own tax complications of Social Security benefits and Required Minimum Distributions). Which means there will be years where a household can ‘time’ its tax situation, by contributing to traditional IRAs in years when income and tax rates are high, and tactically switching to Roth contributions (or even engaging in Roth conversions) when tax rates are unusually low.

Of course, there’s always a risk that tax rates will change in the future, not because of the household’s change in income, wealth, or circumstances, but simply because Congress itself ‘changes the rules’ by altering tax rates. Although, in reality, while tax brackets have varied significantly throughout history, tax deductions have often changed alongside the brackets, such that changes in effective tax rates have actually been remarkably narrow throughout history. In other words, the variability of tax rates due to Congress (which we can’t control) is actually dwarfed by changes in tax rates within the household over time (which can be planned for!).

Ultimately, though, the key point is simply to understand that arbitrarily splitting dollars between traditional and Roth-style retirement accounts isn’t actually a positive wealth-creating strategy; instead, it is more akin to ‘going to cash’ and eliminating the opportunity altogether. For those who want to actually maximize wealth with the traditional-vs-Roth decision, the better approach is to try to Roth-optimize by timing when to shift between traditional and Roth accounts. Which, in practice, is easier than most realize, as while a household’s future is never certain, the Roth-vs-traditional decision has the most impact in years that are especially high or low in income… which are actually the years that are most easy to identify in the moment for a Roth optimization timing decision!